Capitalization and its theories

Understanding Capitalization in Business

Introduction

Every business aims to maximize its value. To achieve this, both finance managers and individual investors need to understand the concept of capitalization. Capitalization essentially refers to the total value of a business, reflecting how it's funded and its worth. It’s a critical aspect of financial management, relevant at all stages of a company's lifecycle.

Concept of Capitalization

Capitalization is the total valuation of a business. It's the sum of all long-term funds invested in the company, including:

- Owned Capital: Money invested by the owners (shareholders).

- Borrowed Capital: Money raised through loans and debt instruments.

More specifically, capitalization is the valuation of long-term funds that have been invested in the business. It represents how a company's long-term financial obligations are distributed between its owners and creditors. In broader terms, it includes owner’s funds, borrowed funds, long-term loans, and any surplus earnings

Understanding Capitalization in Business

Introduction

Every business aims to maximize its value. To achieve this, both finance managers and individual investors need to understand the concept of capitalization. Capitalization essentially refers to the total value of a business, reflecting how it's funded and its worth. It’s a critical aspect of financial management, relevant at all stages of a company's lifecycle.

Concept of Capitalization

Capitalization is the total valuation of a business. It's the sum of all long-term funds invested in the company, including:

Owned Capital:Money invested by the owners (shareholders).Borrowed Capital:Money raised through loans and debt instruments.

More specifically, capitalization is the valuation of long-term funds that have been invested in the business. It represents how a company's long-term financial obligations are distributed between its owners and creditors. In broader terms, it includes owner’s funds, borrowed funds, long-term loans, and any surplus earnings.

Different financial experts define capitalization slightly differently, but the central idea remains consistent: It's the total value of a company's long-term funding.

Definitions by Experts:

- Guthmann and Dougall: Capitalization is the total of the par value of outstanding stocks and bonds.

- Walker and Baughen: Capitalization includes long-term debt and capital stock, rejecting the idea that short-term creditors don't contribute to a company's total capital.

- Bonneville and Deway: Capitalization is the balance sheet value of outstanding stocks and bonds.

In Simple Terms: Capitalization represents the total value of the securities (stocks, bonds, etc.) issued by a company. It’s the sum of what the company owes to its owners and long-term lenders.

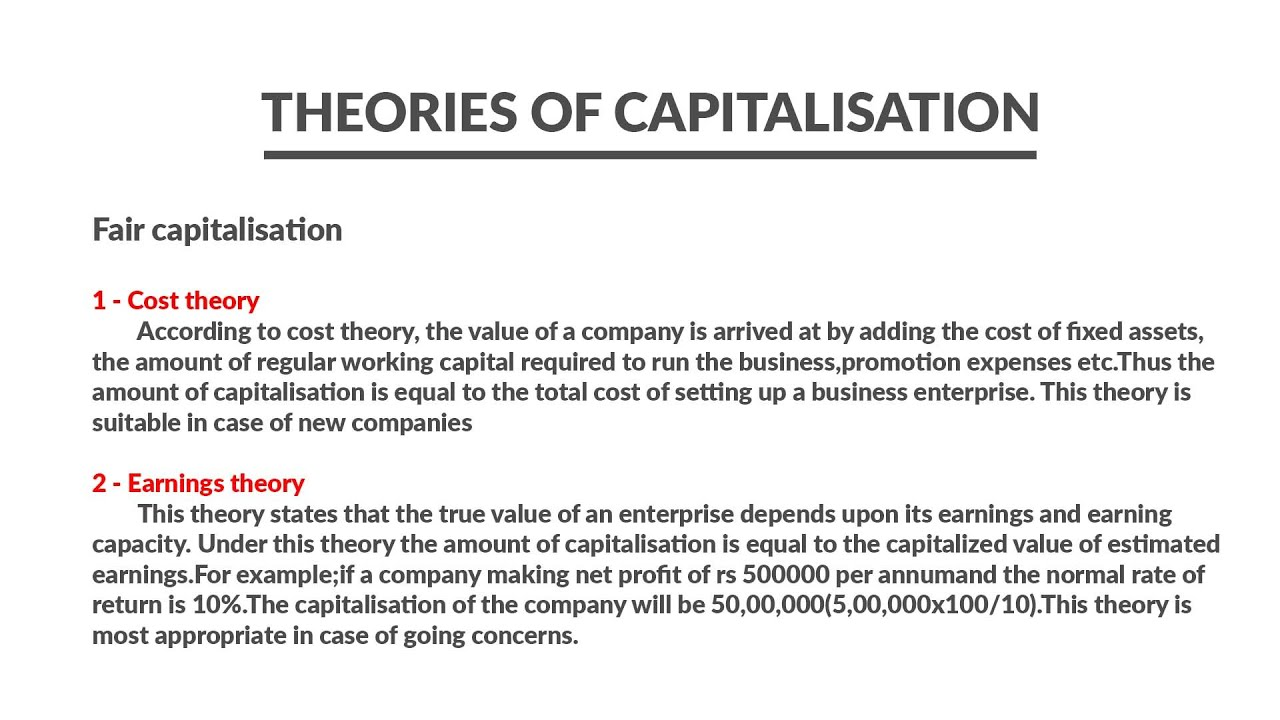

Theories of Capitalization

There are two main theories on how to determine the value of a company through capitalization: the Cost Theory and the Earning Theory.

1. Cost Theory

This theory focuses on the cost of acquiring assets. The total capitalization value is determined by adding up all the costs incurred in acquiring the assets a company uses. These costs include:

- Fixed Assets: Land, buildings, machinery, etc.

- Current Assets: Raw materials, inventory, debtors.

- Preliminary Expenses: Costs associated with starting the business, including expenses for issuing shares or securities.

When it's best used: The Cost Theory is often most useful for new companies because it helps them determine the total amount of capital they need to launch and operate their business.

Limitations:

- Ignores Earning Capacity: The cost theory only looks at what was spent to acquire assets. It does not consider how well those assets are able to produce income.

- Ignores Obsolescence: The cost theory does not take into account the time when the asset may become outdated or no longer useful.

- Not Useful for Fluctuating Earnings: The cost theory doesn't work well for companies that have very inconsistent or changing earnings.

2. Earning Theory

This theory focuses on the earning capacity of the business. It determines the capitalization value based on how much money a company is expected to make. The calculation uses a capitalization rate, which is usually the representative rate of return in the industry.

Calculation:

When it's best used: This theory is generally more relevant for mature companies with a stable history of earnings.

Limitations:

- Difficult to Estimate Future Earnings: For new companies, it can be difficult to accurately estimate future earnings.

- Inaccurate Capitalization Rate: If the capitalization rate is not a proper representation for a firm, then the calculation will be inaccurate.

- Influence of Mistake in Earnings: Any error in the future earnings estimation will have a direct impact on the amount of capitalization value.