Ownership Securities

Business Funds: Understanding Equity, Preference, and Other Share Types

Businesses require a continuous flow of funds to operate and grow. These funds can be categorized based on time period, ownership, control, and source of generation. This document will focus on different types of shares, specifically equity shares, preference shares, and other related concepts.

Core Concepts

- Business Funds: Money required for a business to function.

- Shares: Units into which a company's capital is divided.

- Shareholder: A person holding shares in a company.

Equity Shares (Ordinary Shares)

-

Definition: Equity shares represent fractional ownership in a company. Holders are considered members and bear the maximum business risk.

-

Key Characteristics:

- Ownership Capital: Capital raised through equity is considered ownership capital.

- Voting Rights: Equity shareholders have voting rights and participate in company management.

- Residual Owners: They receive dividends only after all other claims are settled, and dividend payment is not fixed.

- Long-Term Capital: Equity shares are a crucial source of long-term finance.

-

Merits of Equity Shares:

- Foundation of Capital: Provides the base for the company's capital structure.

- Creditworthiness: Enhances the company's credit rating and confidence among lenders.

- High Returns: Attracts investors seeking higher returns (with higher risk).

- No Compulsory Dividend: No legal obligation to pay dividends if the company doesn't profit.

- No Asset Charge: Does not create a charge on the company's assets.

- Democratic Control: Voting rights allow shareholders to have democratic control over management.

-

Limitations of Equity Shares:

- Unstable Income: Not ideal for investors who prefer steady income.

- High Cost: Often the most expensive way for a company to raise funds.

- Dilution of Voting: Issuing new equity dilutes the voting power of existing shareholders.

- Time-Consuming: Involves many legal procedures and delays.

Preference Shares

-

Types of Preference Shares:

-

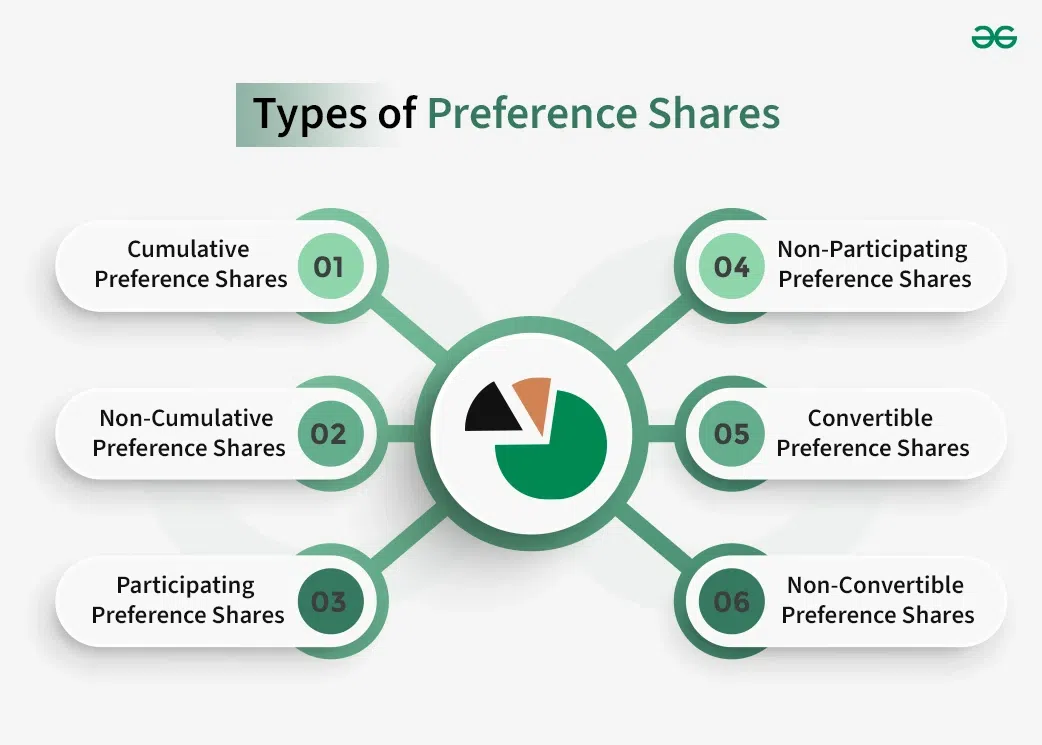

Cumulative vs. Non-Cumulative:

- Cumulative: Unpaid dividends are accumulated for future payment.

- Non-Cumulative: Unpaid dividends are not carried over.

-

Participating vs. Non-Participating:

- Participating: Shareholders have a right to participate in surplus profits after a fixed dividend.

- Non-Participating: Do not participate in surplus profits.

-

Convertible vs. Non-Convertible:

- Convertible: Can be converted into equity shares after a fixed period.

- Non-Convertible: Cannot be converted into equity shares.

-

-

Merits of Preference Shares:

- No Dilution of Control: Do not dilute control over management since they generally lack voting rights.

- Potential Higher Equity Dividends: Can lead to higher rates of dividend for equity shareholders during good times.

- Steady Income: Provides a reasonably stable return to shareholders.

- Safety of Investment: Relatively lower risk than equity shares.

- Preferential Right of Repayment: Priority over equity in the case of liquidation.

- No Asset Charge: Doesn't create any charge against the assets of a company.

-

Limitations of Preference Shares:

- Higher Dividend Cost: Usually carry a higher dividend rate than the interest on debentures.

- Dividend Dependent on Profits: Dividends are not assured, payable only from profits.

- Not Ideal for High-Risk Investors: Not preferred by investors seeking higher returns and willing to take higher risks.

- Dilution of Claims: Preference capital dilutes the claim of equity shareholders over the assets of the company.

- No Tax Benefit: Dividend paid on preference shares is not tax-deductible, unlike interest on loans.

Other Types of Shares

Creditorship Securities

- Definition: Also known as debt finance, these are funds raised from creditors (not through ownership).

- Examples: Debentures and bonds are the main types of creditorship securities.

Key Takeaways

This information provides a fundamental understanding of different share types and their relevance in business financing. When making investment or financing decisions, it's important to carefully assess the characteristics, advantages, and limitations of each type of share.