Place and Time Taxable Under GST

Place and Time of Supply Under GST: Key Concepts for Compliance

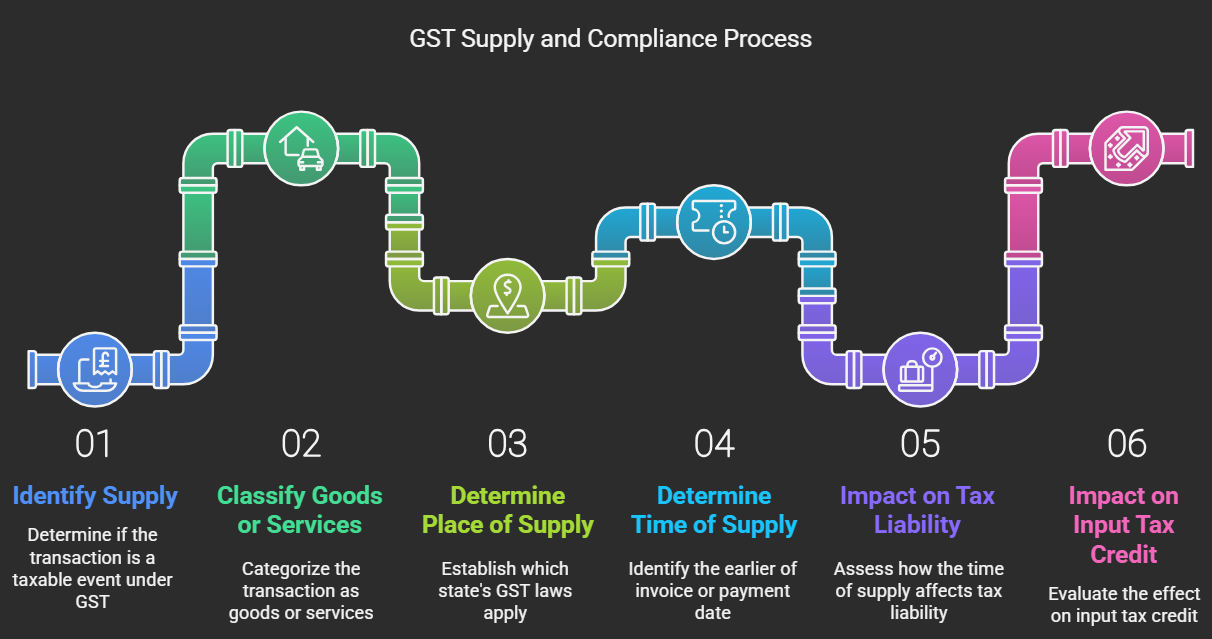

Determining the correct place and time of supply is crucial for accurate GST compliance. These concepts determine where the tax liability arises and when it becomes payable.

By accurately determining the place and time of supply, businesses can ensure compliance with GST regulations, avoid penalties, and maintain accurate tax records.

Concept of Place of Supply

The place of supply determines which state's GST laws apply to a transaction and where the tax revenue should be credited. Since GST is a destination-based consumption tax, the place of supply is generally the location where the goods or services are consumed.

Rules for Determining Place of Supply:

The GST law provides specific rules for determining the place of supply for different types of transactions:

-

Supply of Goods:

- General Rule: The place of supply is the location where the goods are delivered.

- Exceptions: Specific rules apply for goods imported into India, goods supplied through an e-commerce operator, etc.

-

Supply of Services:

- General Rule: The place of supply is the location of the recipient of services.

- Exceptions: Specific rules apply for services related to immovable property, transportation of passengers, online information and database access or retrieval services, etc.

Registered vs. Unregistered Persons:

- Registered Persons: For supplies to registered persons, the place of supply is determined based on the address of the recipient on record.

- Unregistered Persons: For supplies to unregistered persons, the place of supply is generally the location where the supplier makes the supply.

Concept of Time of Supply

The time of supply determines when the liability to pay GST arises. This is crucial for determining the correct tax period for which GST should be paid and for claiming input tax credit.

Determining Time of Supply:

The GST law provides specific rules for determining the time of supply for different types of transactions:

-

Supply of Goods:

- General Rule: The earlier of the date of invoice or the date of payment.

- Exceptions: Specific rules apply for continuous supply of goods, supply of goods where the invoice is not issued within the prescribed time, etc.

-

Supply of Services:

- General Rule: The earlier of the date of invoice or the date of payment, or the date of provision of service if the invoice is not issued within the prescribed time.

- Exceptions: Specific rules apply for continuous supply of services, services provided on board a conveyance, etc.

Significance in GST Compliance

Understanding the place and time of supply is crucial for:

- Determining Tax Liability: It helps businesses determine the correct state where GST is payable and the relevant tax period for payment.

- Claiming Input Tax Credit: The time of supply affects the time period in which input tax credit can be claimed.

- Filing GST Returns: Accurate determination of place and time of supply is essential for filing correct GST returns.

- Avoiding Penalties: Incorrect reporting of place or time of supply can lead to penalties and interest charges.