Behavior of a Firm

- Assume all firms have a common goal of maximizing profit.

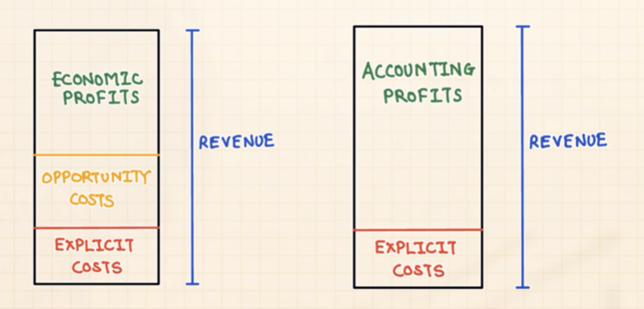

- Revenue = quantity x price

- Explicit costs: All costs incurred during production of the good/service

- Rent, material costs, labor, etc.

- Implicit Costs: Opportunity cost

- Economic profit: Revenue – (Implicit costs + explicit cost)

- Accounting profit: Revenue – Explicit cost

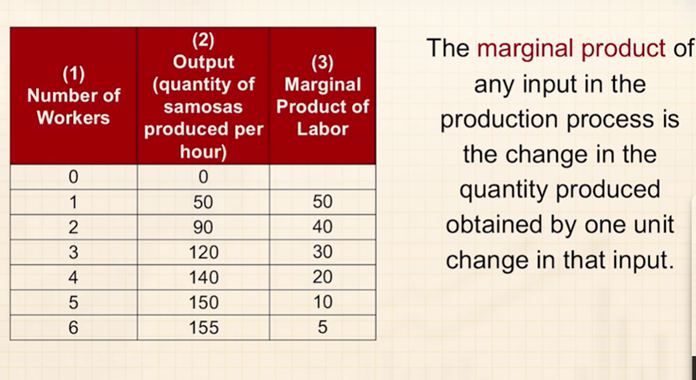

Marginal Product:

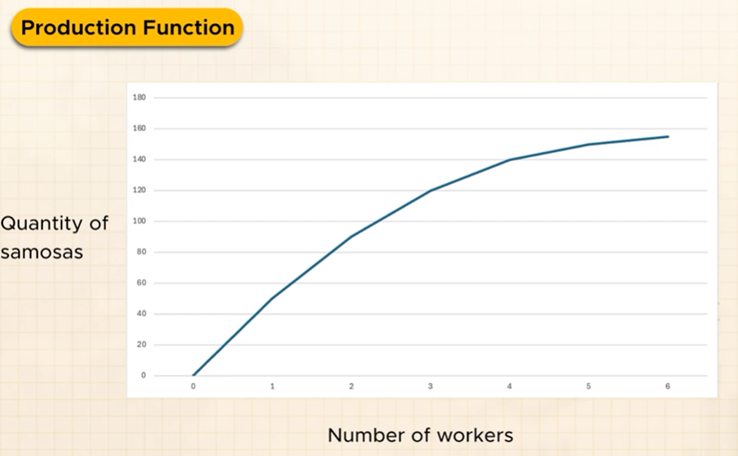

The production curve gets flatter as quantity of labor increases. In this example, it could be because the more number of workers there are, the less access to equipment each worker has.

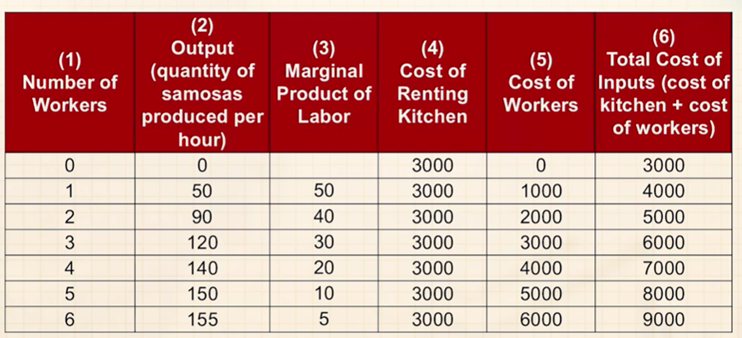

Costs (Elaborated further):

No Comments