Theories of dividend decision , determinants , companies act 2013

IV.

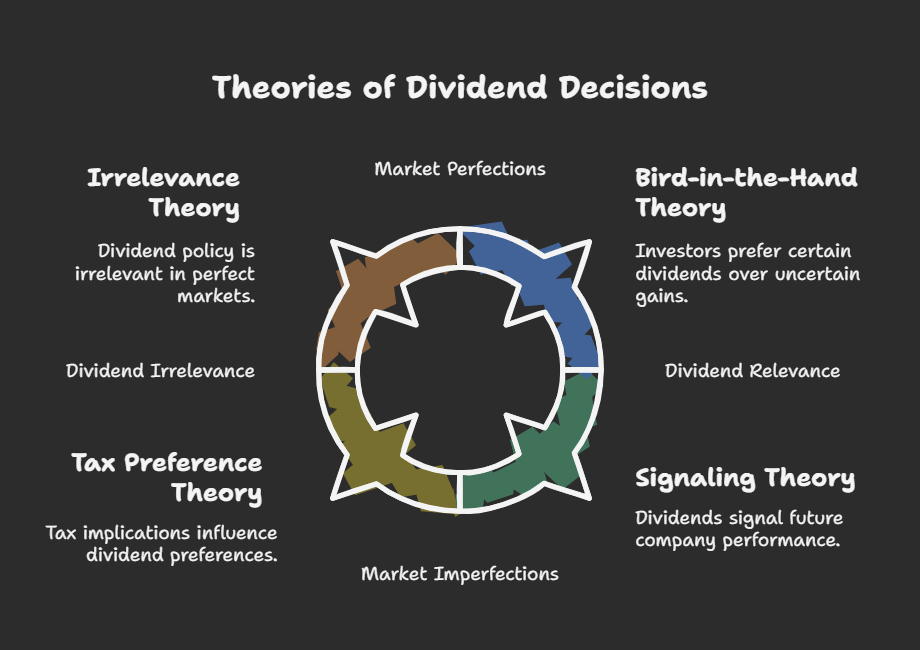

V. Theories of Dividend Decisions

These theories attempt to explain the relationship between dividend policy and the value of the firm.

A. Irrelevance Theory (Modigliani and Miller - MM):

-

Core Idea:

UnderDividend policy is irrelevant under perfect market conditions (no taxes,notransaction costs, perfect information), dividend policy is irrelevant to the value of the firm.. Investors can createtheir own"homemadedividends"dividends." -

selling shares if they need cash, or reinvest dividends if they don't.Assumptions: Perfect markets, rational investors, no taxes, no transaction costs, fixed investment policy.

-

Criticisms:

The realReal world is notperfect.perfect;Taxes,taxes, transaction costs, and information asymmetryexist,exist.

B. Relevance Theories: These theories argue that dividendDividend policy does matter.matters.

- Walter's Model:

-

Core Idea:

The optimalOptimal dividend policy depends on the relationship between the firm's internal rate of return (r) and the cost of capital (k). - If r > k: Growth firm; retain earnings (0%

dividendpayout). - If r = k: Indifference; dividend policy doesn't matter.

- If r < k: Declining firm; pay out all earnings

as dividends(100%dividendpayout). -

ratio is optimal).Formula: P = (D + (E-D) * (r/ke)) / ke

Where:- P = Market Price per

share,share - D = Dividend per

share,share - E = Earnings per

share,share - r = firm's rate of

return,return - ke = Cost of Equity Capital

- P = Market Price per

-

Core Idea:

The valueValue ofastock is the present value ofitsexpected future dividends. -

Formula: P0 = D1 / (ke - g)

Where:- P0 = Current

price,price - D1 = Expected dividend next

year,year - ke = Required rate of

return,return - g = Constant growth rate of

dividends.dividends

- P0 = Current

-

Implication: Higher dividends and

a highergrowthrate of dividends lead to a= higher stock price. -

Criticisms: Assumes

aconstant growth rate,which is not always realistic. Also verysensitive totheinputs (ke and g).

-

Core Idea: Investors prefer current dividends (

a"bird in the hand") over uncertain future capital gains. -

Rationale: Dividends reduce

uncertaintyuncertainty. -

future returns.Implication: Higher dividends

lead to a= higher stockprice,price. -

if the total return is the same.Criticisms: Contradicts

theMM irrelevance theory.

C. Tax Preference Theory:

-

Core Idea: Dividend policy

isinfluenced bythetax implications for investors. -

Rationale: If dividends

aretaxedat ahigherratethan capital gains, investorsmayprefercompaniesretainedthatearnings. -

earnings and generate capital gains. Conversely, if dividends are taxed at a lower rate, investors may prefer higher dividend payouts.Empirical Evidence:

Evidence is mixed, asMixed, tax lawsvaryvary.

D. Signaling Theory (Dividend Signaling):

-

Core Idea: Dividends convey information about

a company'sfuture prospects. -

Rationale: Management has inside

informationinformation. -

theImplication:company's profitability.Implication: A dividendDividend increase is a credible signalthat management expectsof higher future earnings.A dividendDividend decrease isanegative.

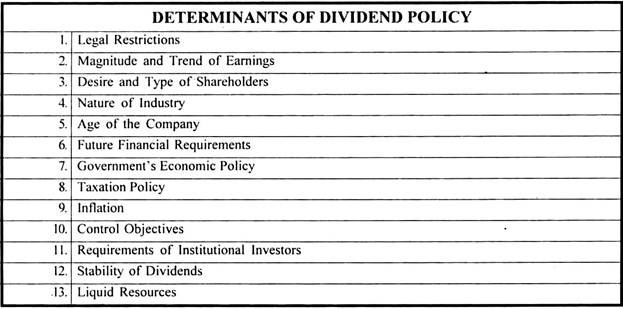

V. Determinants of Dividend Policy Decisions

-

thatProfitability:influence a company's dividend policy:Profitability: A company needs sufficientSufficient profits to pay dividends. -

Liquidity:

Even if profitable, a company must have sufficientSufficient cashtofordistributedistribution. -

Investment Opportunities:

CompaniesAttractivewith attractive investment opportunitiesprojects maychooselead toretainretainingearningsearnings. -

fund those projects.Financial Leverage (Debt): High debt

levelsmay restricta company's ability to pay dividends. Creditors may impose restrictions ondividend payments. -

Growth Rate: High-growth companies often retain

earningsearnings. -

finance growth. -

Legal Restrictions: Companies Act and other

regulationsregulations. -

Contractual Restrictions: Loan agreements may restrict

dividendpayments. -

Contractual Restrictions: Loan agreements or bond indentures may restrict dividend payments.Inflation: High inflation

will reduce thereduces real value ofdividendsdividends,andrestrictinghencepolicy. -

policy becomes restrictive.Stability of Earnings: Stable

earningearningscompanies tendlead topayhigherapayouts. -

dividend payout ratio.Access to Capital Markets:

Companies with readyEasy accesstoencouragescapitaldistribution. -

tend to distribute earnings in the form of dividend.Control Objective:

IfStockmanagement wants todividends maintaincontrolcontrol. -

theTaxation:company, they may declare stock dividend instead of cash dividends.Taxation: Taxation policy has a significantSignificant effect onthedividendpolicypolicy.

Factors

VI. Companies Act, 2013 and SEBI Guidelines on Dividend Distribution (Theory Only)

A. Companies Act, 2013 (Key Provisions):

-

Section 123:

Deals with the declarationDeclaration of dividends.Dividends- Out

onlyofbecurrentdeclaredprofits,out of:Current profits.Pastpast accumulatedprofits (undistributed profits).Money provided by the Centralprofits, orStatemoneyGovernmentfromforgovernment. - Depreciation must be provided

forfor. - Board

may decide tocan transfera portion of theprofits toreservesreserves. - Inadequacy of

inadequacy of profits,profits: dividends can be declaredout offrom accumulated profits subject tocertainrules.

canthe payment of dividends.before declaring dividends.Transfer to Reserves: Thebefore declaring dividends.In caseconditionsand - Out

-

Section 124:

Deals with theUnpaid Dividend Account.Dividends- Unpaid/unclaimed

remain unpaid or unclaimeddividends within 30 daysmust be transferredgo toanUnpaid Dividend Account. - Unclaimed for 7 years,

it must betransferred totheInvestor Education and Protection Fund (IEPF).

thatIf the amount remains unclaimed - Unpaid/unclaimed

-

Interim Dividend:

TheBoardof Directors maycan declare interimdividendsdividends.

B. SEBI (Securities and Exchange Board of India) Guidelines on Dividend Distribution (Listed Companies):

- Listing Agreement/Regulations:

SEBI regulations mandate certainMandates disclosures andproceduresprocedures. -

dividend distribution by listed companies.Disclosure Requirements:

Companies- Dividend amount, record date, payment

date,date. - Reasons for

anychanges inthepolicy.

must disclose the dividendand other relevant information to the stock exchanges.Must disclose the reasonsdividendpolicy. - Dividend amount, record date, payment

-

Record Date:

The company must announce theAnnounce record date fordeterminingeligibility. -

eligiblePayment Timeline: Adhere toreceive dividends.Payment Timeline: Companies must adhere to a prescribedtimelinefor dividend paymentsafter declaration. -

Dividend Warrants/Electronic Transfer:

DividendsPaymentcanmethods. -

paid via dividend warrants or electronic transfer to shareholders' bank accounts.Compliance with Accounting Standards: Dividend distribution must

becomply. -

compliance with applicable accounting standards.Regulations for Bonus Issues:

SEBISpecifichasregulations.

Important Considerations:

- Practical Application:

DividendComplexpolicy is a complex area. Companies mustarea; considera wide range of factors, including theirfinancial situation,investmentopportunities, and shareholder preferences. - Dynamic Nature:

Dividend policy is not static. Companies should review their dividend policy periodicallyReview andmakeadjustadjustmentsperiodically. - Consultation:

Companies should consultConsult withfinancialadvisors and legalcounselcounsel.

This detailed overview should provide a comprehensive understanding of dividend policy decisions. Remember to consult specific legal and regulatory documents for the most up-to-date information. Good luck!