Administrative Framework

Administrative Framework of GST in India

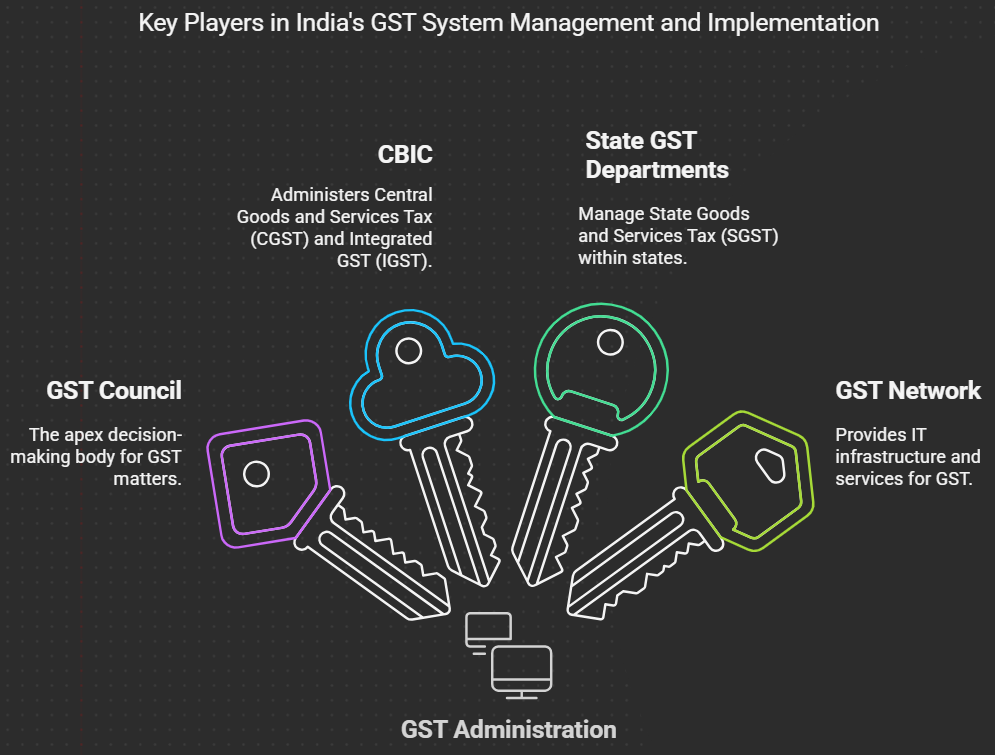

Administration of GST

The administration of GST in India is a collaborative effort between the central and state governments. It involves various bodies working together to ensure the smooth implementation and operation of the GST system.

- GST Council: The apex body for decision-making on GST matters.

- Central Board of Indirect Taxes and Customs (CBIC): Responsible for administering CGST and IGST at the central level.

- State GST Departments: Responsible for administering SGST within their respective states.

- GST Network (GSTN): A non-profit, non-government organization that provides the IT infrastructure and services for the GST system.

GST Council

The GST Council is a constitutional body established under Article 279A of the Constitution of India. It is the key decision-making body for all GST-related matters.

Formation:

- The GST Council was formed after the 101st Constitutional Amendment Act, 2016.

- It was constituted by the President of India within 60 days of the commencement of Article 279A.

Composition:

- Chairperson: Union Finance Minister

-

Members:

- Union Minister of State in charge of Revenue or Finance

- Minister in charge of finance or taxation of all the States

Powers and Functions:

The GST Council is empowered to make recommendations to the Union and State Governments on various GST-related matters, including:

- Taxes, cesses, and surcharges: Recommending which taxes should be subsumed under GST.

- Goods and services: Deciding which goods and services should be subject to or exempt from GST.

- GST laws: Formulating model GST laws, principles of levy, and apportionment of GST.

- Threshold limits: Determining the threshold limit for GST registration.

- GST rates: Recommending GST rates, including floor rates with bands.

- Special rates: Proposing special rates during natural calamities or disasters.

- Special provisions: Recommending special provisions for certain states (North Eastern states, Himachal Pradesh, Jammu and Kashmir, and Uttarakhand).

- Compensation to states: Recommending compensation to states for revenue loss due to GST implementation.

Decision-Making:

- Decisions in the GST Council are taken by a majority of not less than three-fourths of the weighted votes of the members present and voting.

- The vote of the Central Government has a weightage of one-third of the total votes cast.

- The votes of all the State Governments together have a weightage of two-thirds of the total votes cast.

Significance:

The GST Council plays a crucial role in the successful implementation of GST in India. It ensures cooperative federalism by bringing together the central and state governments to make decisions on GST-related matters. The Council's recommendations have helped to create a unified and efficient indirect tax system in India.

No Comments