Provisions-Conditions-Utilization of CGST, SGST, UTGST and IGST-Capital Goods

Input Tax Credit (ITC) and GST Liability

1. Introduction

The Goods and Services Tax (GST) system in India consists of four key components:

- CGST (Central Goods and Services Tax) – Levied by the central government on intra-state supplies.

- SGST (State Goods and Services Tax) – Levied by the state government on intra-state supplies.

- UTGST (Union Territory Goods and Services Tax) – Levied by union territories without legislatures.

- IGST (Integrated Goods and Services Tax) – Levied on inter-state supplies.

GST provides a structured approach to claiming and utilizing ITC across CGST, SGST, UTGST, and IGST. Adhering to the provisions, conditions, and timelines ensures compliance and maximizes tax benefits for businesses.

2. Provisions of CGST, SGST, UTGST, and IGST

Central Goods and Services Tax (CGST) Act, 2017

- CGST is levied by the central government on intra-state supplies.

- Rates are determined by the GST Council.

- ITC can be utilized against CGST and IGST.

State Goods and Services Tax (SGST) Act, 2017

- SGST is levied by the respective state governments on intra-state supplies.

- Rates are uniform across states as decided by the GST Council.

- ITC can be utilized against SGST and IGST but not CGST.

Union Territory Goods and Services Tax (UTGST) Act, 2017

- Applicable in union territories such as Chandigarh, Lakshadweep, etc.

- Functions similar to SGST but applicable in union territories.

Integrated Goods and Services Tax (IGST) Act, 2017

- IGST is levied on inter-state transactions.

- Administered by the central government but shared with the states.

- ITC can be utilized against IGST, CGST, and SGST.

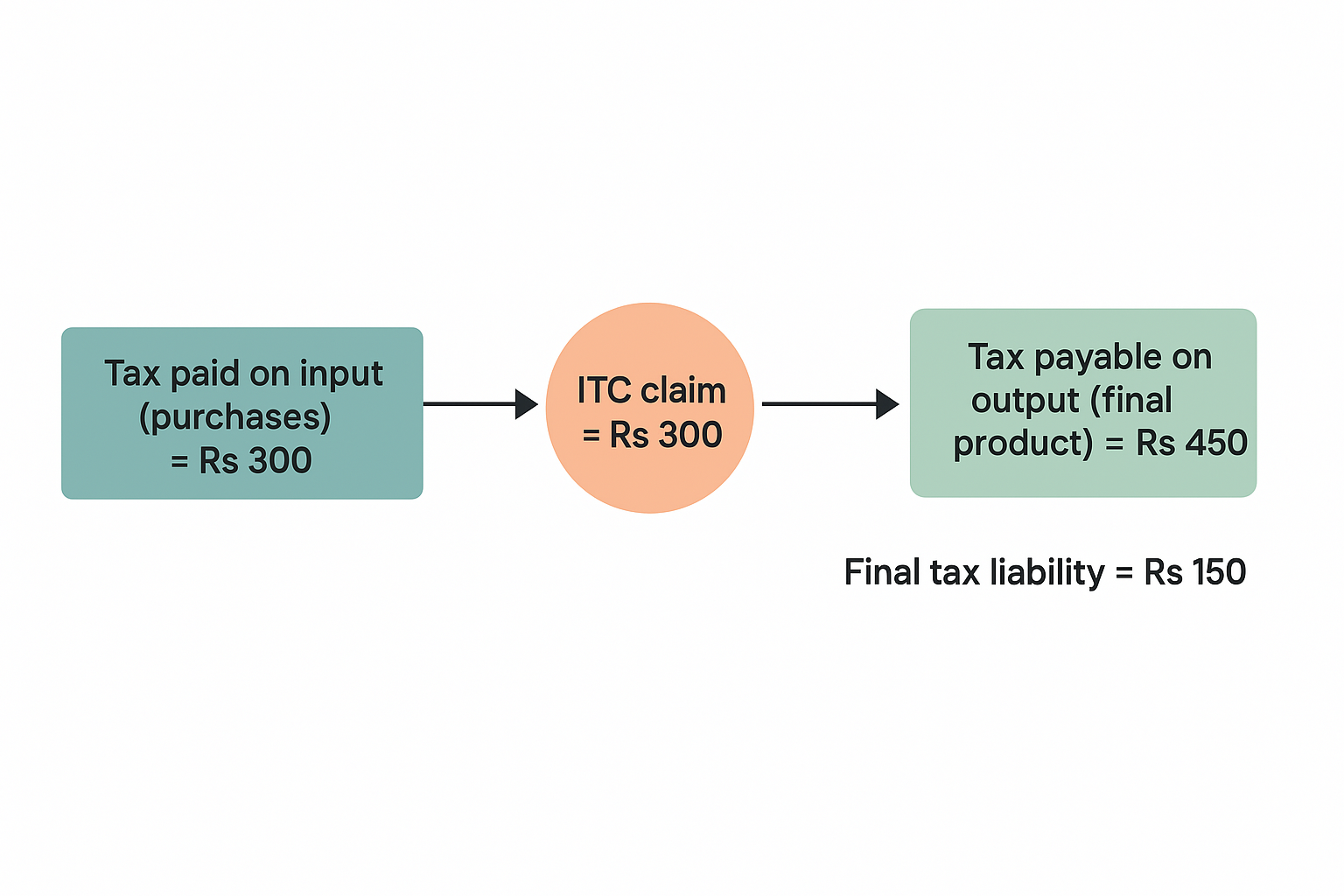

3. What is Input Tax Credit (ITC)?

Input Tax Credit (ITC) allows businesses to reduce the tax paid on purchases from the tax payable on sales. The mechanism ensures that tax is paid only on the value addition at each stage.

For example:

- Tax payable on output (final product) = Rs 450

- Tax paid on input (purchases) = Rs 300

- ITC claim = Rs 300, thus final tax liability = Rs 150

4. Conditions for ITC Claim under GST

To claim ITC, businesses must fulfill the following conditions:

- Must be registered under GST.

- Must have a valid tax invoice from a registered supplier.

- Goods/services must have been received.

- The supplier must have paid the tax to the government.

- The recipient must have filed GSTR-3B.

- Payment towards invoice must be made within 180 days.

- ITC must be claimed within the time limit:

- 30th November of the following financial year, or

- Before filing the annual return, whichever is earlier.

5. Utilization of CGST, SGST, UTGST, and IGST

GST law prescribes a set-off mechanism:

| Tax Type | Can be used to pay | Order of Utilization |

|---|---|---|

| CGST | CGST & IGST | 1. CGST first, then IGST |

| SGST/UTGST | SGST/UTGST & IGST | 1. SGST/UTGST first, then IGST |

| IGST | IGST, CGST, SGST/UTGST | 1. IGST first, then CGST, then SGST/UTGST |

6. Eligible and Ineligible ITC

Under Section 17(5) of the CGST Act, ITC cannot be claimed on certain goods/services:

Ineligible ITC

- Motor Vehicles (except for resale/commercial use).

- Food & Beverages, Catering, Health Services (unless legally mandated).

- Membership Fees (e.g., clubs, gyms).

- Insurance (except for government mandates).

- Construction Expenses (for immovable property).

- Lost, Destroyed, or Gifted Goods.

7. Documents Required for ITC Claim

To claim ITC, businesses need:

- Invoice issued by the supplier.

- Debit notes issued by the supplier.

- Bill of entry for imports.

- Credit note issued by Input Service Distributor (ISD).

- A bill of supply issued for purchases under the composition scheme.

8. ITC on Capital Goods

What are Capital Goods?

Capital goods are assets used for business, such as machinery, equipment, and tools. ITC is available for capital goods unless:

- They are used exclusively for exempt supplies.

- They are used for personal purposes.

- Depreciation is claimed on the tax component of capital goods.

9. ITC for Job Work

- ITC is allowed for principal manufacturers who send goods for job work.

- Goods must be received back within 1 year (or 3 years for capital goods).

10. ITC by Input Service Distributor (ISD)

- The head office or any registered branch can distribute ITC to units.

- ITC is distributed under CGST, SGST/UTGST, or IGST as applicable.

11. ITC on Business Transfer (Mergers & Amalgamations)

- ITC can be transferred in case of business mergers, acquisitions, or amalgamations.

- The transferee can continue to utilize the ITC available to the transferor.

12. ITC for Banks and Financial Institutions

- Banks and financial institutions can claim only 50% ITC on inputs, capital goods, and input services.

- The 50% restriction is due to their exempt financial services.

13. Time Limit to Claim ITC

ITC must be claimed within:

- 30th November of the following financial year, or

- Before filing the annual return, whichever is earlier.

Example: An invoice dated 30th December 2023 can be claimed before 30th November 2024.

14. How to Claim ITC?

- ITC must be reported in GSTR-3B (Table 4).

- Reconciliation with GSTR-2B and the purchase register is mandatory.

- Mismatched ITC claims may lead to penalties and notices.

15. Matching and Reversal of ITC

- ITC claims in GSTR-3B must match with GSTR-2B.

- Ineligible ITC must be reversed in Table 4(B) of GSTR-3B.

- Government audits & real-time scrutiny ensure compliance.

16. Computation of GST Liability

- Net GST payable = Output GST - ITC claimed.

- Errors in ITC reconciliation can lead to additional tax liability.

- Businesses must maintain accurate records to avoid penalties.

No Comments