Reverse Charge Mechanism (RCM)

Reverse Charge Mechanism (RCM) under GST

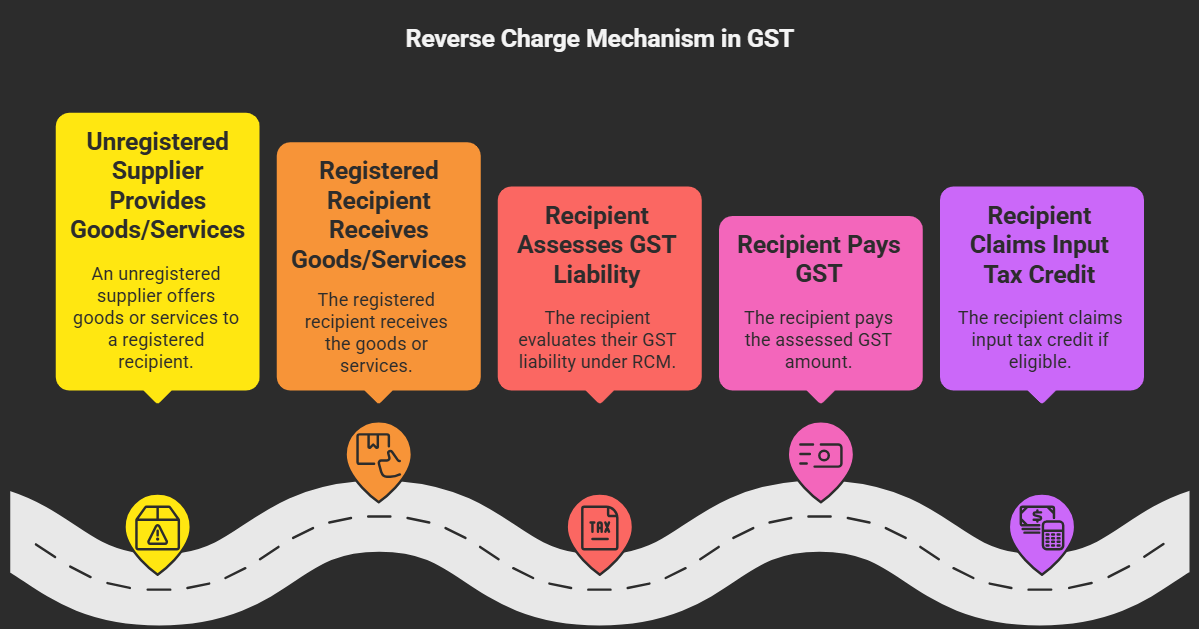

The Reverse Charge Mechanism (RCM) is a special provision under GST where the recipient of goods or services, instead of the supplier, is liable to pay the tax. This mechanism is applied in specific situations to prevent tax evasion and ensure compliance.

What is the Reverse Charge Mechanism?

In the regular GST system (forward charge), the supplier of goods or services is responsible for collecting GST from the recipient and depositing it with the government. However, under RCM, this liability shifts to the recipient.

Significance of RCM

- Preventing Tax Evasion: RCM is often applied when the supplier is unregistered or belongs to a sector prone to tax evasion. By making the recipient liable, the government ensures that tax is collected even if the supplier fails to deposit it.

- Widening the Tax Base: RCM brings certain transactions under the GST ambit that might otherwise escape taxation, such as services provided by unregistered persons.

- Level Playing Field: It creates a level playing field between registered and unregistered suppliers by ensuring that GST is paid even when services are procured from unregistered persons.

Situations Where RCM is Applicable

RCM is applicable in the following situations:

- Supply from Unregistered to Registered Person: When an unregistered person supplies goods or services to a registered person, the registered recipient is liable to pay GST under RCM.

-

Specified Goods or Services: The government has notified certain goods and services where RCM is applicable, even if the supplier is registered. Some examples include:

- Legal services provided by an individual advocate to a business entity.

- Services provided by an insurance agent to an insurance company.

- Supply of goods through an e-commerce operator.

- Import of Services: When a business imports services from outside India, it is liable to pay GST under RCM.

How RCM Works

- Recipient Pays GST: The recipient of the goods or services is liable to pay the GST.

- Self-Assessment: The recipient needs to self-assess the GST payable on the transaction.

- GST Payment: The recipient deposits the GST with the government through their regular GST returns.

- Input Tax Credit: If eligible, the recipient can claim input tax credit for the GST paid under RCM.

Impact on Businesses

RCM can have a significant impact on businesses, especially those that procure services from unregistered suppliers or deal in goods or services covered under RCM. Businesses need to:

- Be Aware of RCM Provisions: Understand the situations where RCM applies.

- Comply with RCM Requirements: Self-assess and pay GST under RCM when applicable.

- Maintain Proper Records: Keep accurate records of RCM transactions for claiming input tax credit and ensuring compliance.

No Comments