Skip to main content

Budgeting Process

What is Budgeting?

-

Budgeting is a structured planning process developed over time.

- It involves all departments and functions within the organization.

- It ensures that departmental goals align with organizational objectives, reducing internal conflicts.

Master Budget

- The final output of the budgeting process.

- A comprehensive blueprint of all planned activities for the year.

- Divided into:

-

Operational Budgets

-

Financial Budgets

1. Operational Budgets

- Expressed in units and monetary value.

- Examples:

-

Sales Budget

-

Production Budget

-

Purchases Budget

-

Labour Budget

-

Overhead Budget

-

Selling & Distribution Expenses Budget

2. Financial Budgets

- Aggregates monetary details from operational budgets.

- Examples:

-

Cash Budget

-

Capital Expenditure Budget

-

Projected Balance Sheet

-

Income Statement

-

Cash Flow Statement

Interdependence of Budgets

- All budget components are interlinked.

- A change in one affects others.

- The process typically starts with identifying the key factor (limiting factor).

Key Factor in Budgeting

- The limiting resource or constraint that influences all other budgets.

- Varies by industry:

-

Sales or Demand → Most common in manufacturing

-

Production Capacity → If machine or manpower is limited

-

Raw Material Availability → In industries like power or pharma

-

Consultant Hours → In professional service firms

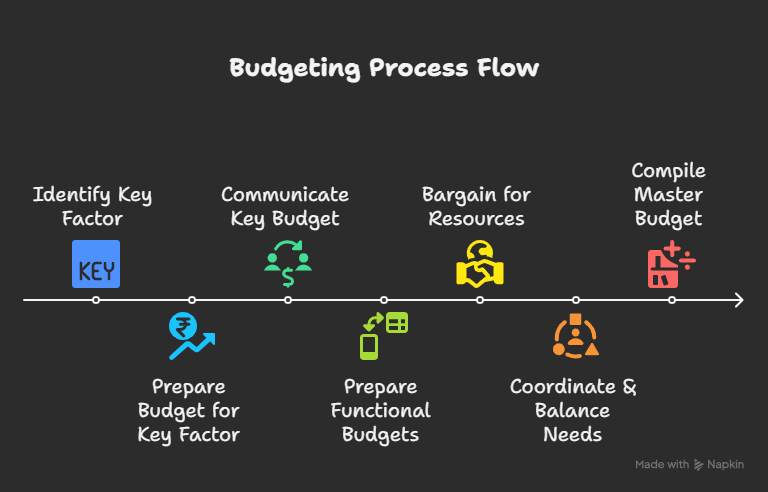

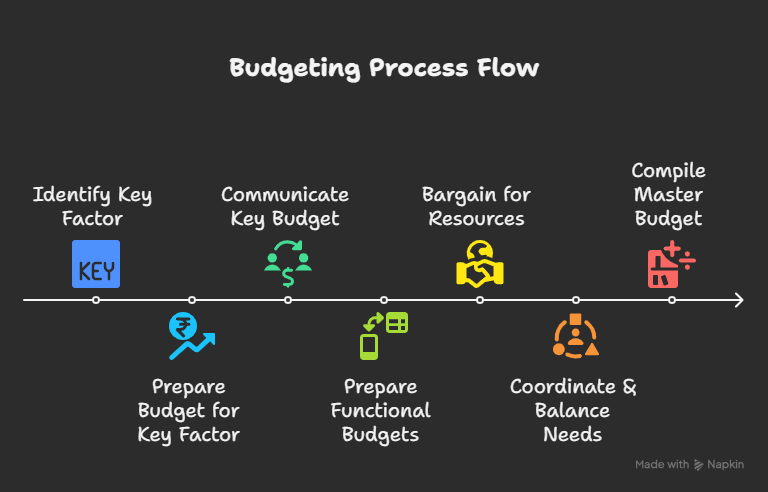

Budgeting Process Flow

-

Identify the Key Factor

-

Prepare Budget for Key Factor

-

Communicate Key Budget to Other Divisions

-

Functional Budgets Prepared in Alignment

-

Departments Bargain for Limited Resources

-

Budget Committee Coordinates & Balances Needs

-

Final Master Budget Document is Compiled

- Expected or Planned Sales (Units & Value)

-

Opening & Closing Inventory:

- Raw Material

- Work-in-Progress (WIP)

- Finished Goods

-

Production Schedule

-

Input Requirements:

- Raw Materials

- Labour

- Machine Hours

- Overheads

-

Indirect Costs (Cost Drivers)

-

Credit Policies (For both sales & purchases)

-

Capital Budgeting Proposals

-

Financial Policies & Forecasts:

- Balance Sheet

- Income Statement

- Cash Flow Statement

No Comments