Types of Budgets

📌 Why Different Types of Budgets?

Organizations face different operational needs, resource constraints, and external uncertainties.

To address this, multiple budgeting approaches are adopted, each with a distinct purpose.

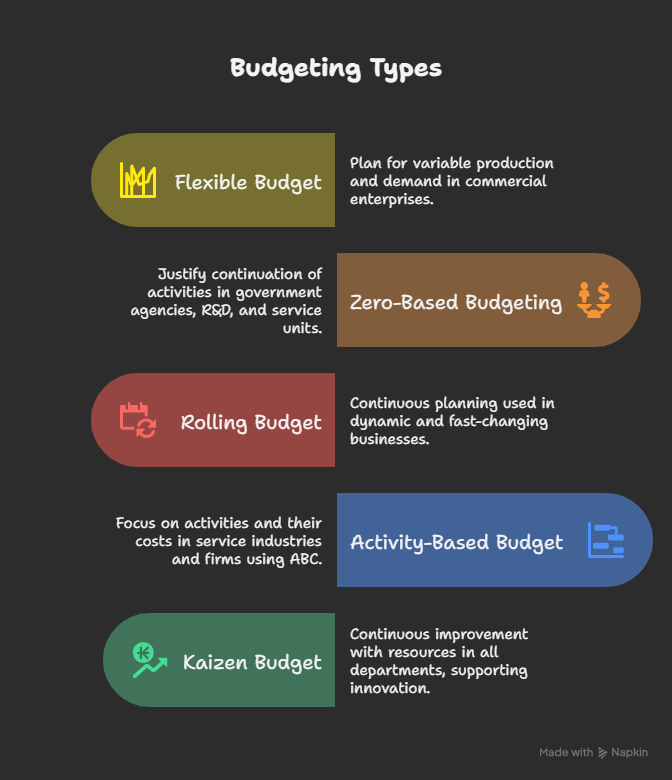

1. Flexible Budget

- Used when there is high demand or production volatility.

- Allows budgeting at various capacity levels without redoing the full process.

- Common in commercial enterprises.

- Example: Budget for 60%, 80%, and 100% utilization scenarios.

2. Zero-Based Budgeting (ZBB)

- Every budget cycle starts from scratch (zero base).

- Continuity of each activity must be justified, regardless of past allocation.

- Common in:

- Government projects (e.g., yearly evaluation of a 5-year polio campaign).

- R&D functions and service departments in private companies.

- Promotes discipline and accountability in budgeting.

3. Rolling or Continuous Budget

- Budget is updated periodically (e.g., quarterly) to cover the next 12 months.

- Encourages budgeting as an ongoing, integrated process.

- Helps adapt to changing business conditions throughout the year.

4. Activity-Based Budgeting (ABB)

- Based on the Activity-Based Costing (ABC) approach.

- Useful when conventional input-based budgeting fails (especially for service firms).

- Focuses on cost of activities, not just inputs like raw material or labour.

-

Steps in ABB:

- Identify activities and calculate cost per activity.

- Estimate demand for activities based on targets.

- Compute budgeted cost of each activity.

- Consolidate into a total budget.

5. Kaizen Budgeting

- “Kaizen” = Continuous improvement.

- Every department must present:

- Planned improvements

- Resources needed (training, equipment, etc.)

- Budget performance is measured by:

- Achievement of targets

- Improvements made

- Makes budgeting forward-looking and development-oriented.

Combining Budgeting Approaches

Different budgets can be used together to enhance effectiveness:

- Zero-Based + Flexible Budget → For departments like R&D or Branding

- Kaizen Budgeting → Can be added to any type of budget

- Activity-Based Budgeting + Flexible Budget → Prepare flexible budgets for each activity

No Comments